Just a reminder that the RAA drought infrastructure loans are still available (and will be until the funding is exhausted).

The loan can be used to:

Max borrow amount: $1m

Interest rate: 2.5% fixed

Term: 20 years

If you need assistance to apply, please contact our office.

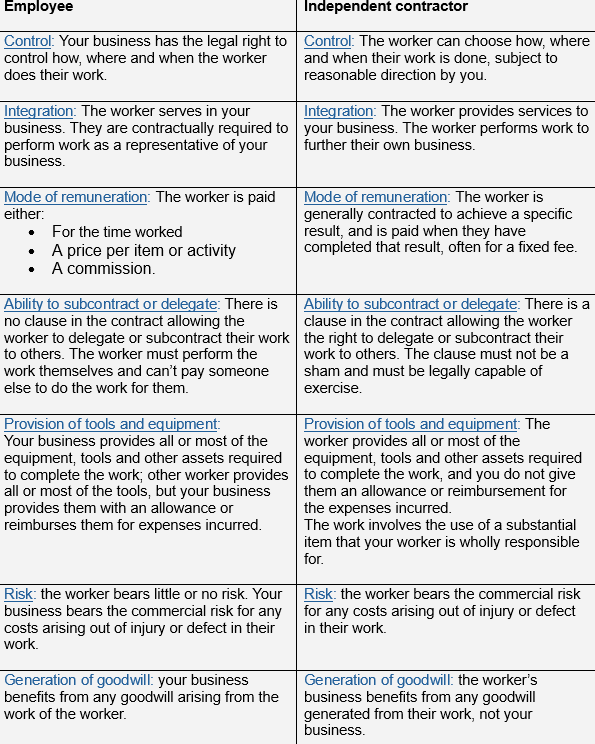

Most businesses that employ contractors understand there is a risk that a contractor may actually be deemed an employee by the ATO.

For example, a business has engaged a contractor for several years, they have paid the contractor their hourly rate but have never paid superannuation or other employee benefits. The ATO reviewed the arrangement and decided that, applying the “multifaced test” the contractor is actually an employee. The business will be liable to pay the contractor several years of superannuation and other employment benefit payments.

The employee v’s contractor relationship can also be challenged by fair work. If a contractor is injured at work, they may not have their own workers compensation insurance policy in place. They may be advised that they should challenge their employer and prove that they are, in fact, a deemed employee and should be covered by the employer’s workers compensation policy. This may create a significant liability for the employer.

The test to define the difference between a contractor and an employee were well established (until now).

A recent High Court judgment in CFMMEU v Personnel Contracting [2022] has confused the employee v contractor relationship again. In the case the court diverted from the above multifaceted tests. Instead, they examined the written contract between the employer and contractor. The contract clearly stated that the relationship was one of a contractor (although applying the multifaceted test suggested the relationship was one of an employee). The court found that the relationship was that of a contractor – because that’s what the contract said.

It is becoming more difficult for clients to manage their contractor risk. Our suggestion is to offer employment to any long-term contractors to minimise risk. It seems this issue is one of, "everything is right… until its not."

Australians love property and the lure of a 15% preferential tax rate on income during the accumulation phase, and potentially no tax during retirement, is a strong incentive for many SMSF trustees to dream of large returns from property development

https://www.ato.gov.au/newsrooms/smsf-newsroom/smsfs-investing-in-property

“…no matter what life throws at you, seek out opportunities to contribute, to participate and to action change….have a crack, and as I like to say, don’t just lean in, leap in.”

Joint Australian of the Year 2024 Richard Scolyer